States Are Passing Laws Compelling Financial Institutions to Honor Donors’ Charitable Bequests

Newsletter

June 15, 2026

Share

Five states have now passed laws mandating that financial institutions promptly distribute funds and assets left to charities and prohibiting the financial custodian from requiring charities to open accounts and/or turn over personal identifiable information (PII) of their executives.

April 2026 was an important month for charitable gift planning. Colorado Governor Jared Polis signed SB26-118 into law, Tennessee Governor Bill Lee signed HB2112 / SB2642, and Nebraska Governor Jim Pillen followed just days later signing LB758, making Nebraska the fifth state to enact these measures to protect both donors and the organizations they support.

These legislative solutions have evolved from an initiative branded the RIFT Project, led by Attorney Johni Hays of Thompson & Associates. RIFT stands for Release IRA Funds Timely. These laws require financial institutions to pay proceeds left in beneficiary designations, transfer-on-death (TOD) and pay-on-death (POD) proceeds — including from IRAs, 401(k)s, and similar accounts — to charities without erecting bureaucratic obstacles, compromising PII, and delaying or diverting donors’ final wishes.

If you work in planned giving, you likely already know the problem these laws are aiming to solve. If you work in finance for a charity, read on.

The Problem That RIFT Laws Address

The so-called “IRA problem” — where financial institutions withhold bequeathed funds and assets, demanding that charitable beneficiaries open new accounts, become a new customer, and produce extensive sensitive personal identifiable information (PII) — has plagued nonprofit gift recipients for decades.

The PII demanded in exchange for releasing clearly bequeathed funds often includes a nonprofit executive’s date of birth, government-issued ID, Social Security number, and personal home address — precisely the kind of sensitive data that individuals are rightly reluctant to share given the risks of fraud, cybersecurity compromise, and identity theft.

Naturally, non-profit leaders’ hesitation to provide this information leads to objections, delays, and in some cases outright denials.

Some financial custodians attribute this practice to their reading of the USA PATRIOT Act of 2001. Others rely on federal rules and regulations from FinCEN and FINRA. And still others, including a handful of the nation’s larger custodians, do promptly release funds to charities, acknowledging that doing so is compliant with applicable law. The problem is persistent while the stated reasons are inconsistent.

In some cases, accounts lie dormant until they are absorbed into state unclaimed property registers, and the charity only learns of them when a recovery firm offers to help (for a 25% fee).

RIFT laws take direct aim at these obstacles, establishing clear, enforceable timelines and removing the compliance barriers institutions have historically erected.

What the New Laws Require

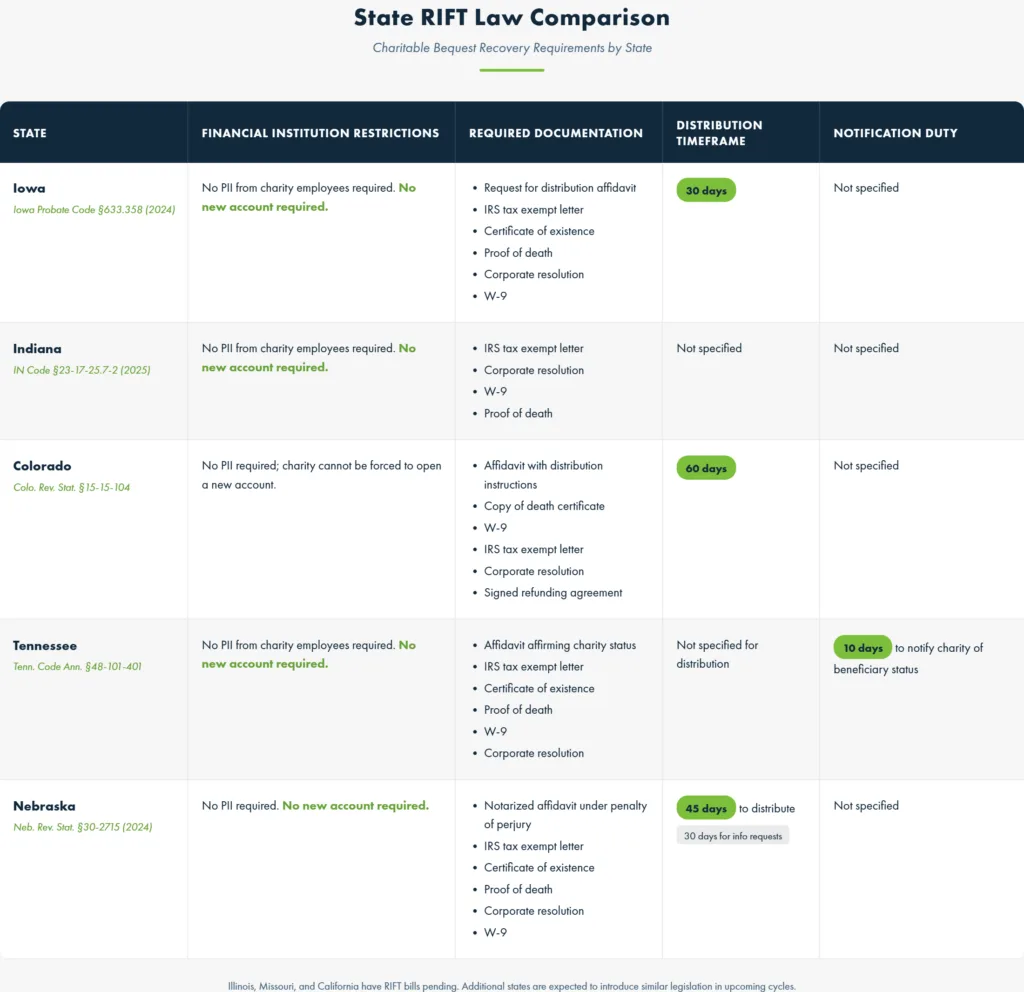

Iowa, Indiana, Colorado, Tennessee, and Nebraska all have enacted RIFT laws. Below are some of the notable elements of each.

Note that these summaries are significantly paraphrased. The new laws create highly specific processes and will require active oversight and facilitation from your organization to take advantage of them.

Financial institutions prohibited from requiring charitable organizations to provide PII of charity employees to obtain gifts or assets bequeathed to the charity.

Charities may, instead, provide the following:

A request for distribution that includes the following information:

Decedent’s name and last known address;

Description of property if known;

Charity name, address, contact information;

Request that the property be paid or transferred to the charity;

That no other individual has a right to the interest in the listed property;

Signed by an authorized individual from the charity.

IRS Tax Exempt Letter

Certificate of Existence from charity’s Secretary of State

Proof of death (death certificate, probate notice, proof of payment of funeral expenses, or obituary of decedent)

Corporate resolution showing signatory’s authority to make the request for distribution

W-9

Upon submission of the required materials, the holding institution must distribute the property within 30 days.

Financial institutions prohibited from requiring charitable organizations to provide PII of charity employees, or to open a new account with the institution, to obtain gifts or assets bequeathed to the charity.

Charities may, instead, provide the following:

IRS Tax Exempt Letter

Corporate Resolution authorizing acceptance of transferred funds

Financial institutions prohibited from requiring a charity to open a new account within the institution or PII in order to receive bequeathed assets. The financial institution must pay or transfer bequeathed assets to the designated charitable beneficiary within sixty days following the submission of the following documents:

An affidavit that includes the following information:

Donor’s name and last known address;

General description of benefits;

Charity name, address, phone number, and website if any;

Instructions on how to distribute assets;

Statement that the information in the affidavit is true and correct;

Signed by a duly authorized representative of the charitable organization;

Copy of death certificate;

W-9;

IRS Tax Exempt Letter;

Corporate resolution

A signed refunding agreement including the terms listed here.

Tennessee – Tennessee Code Annotated, Title 48, Chapter 101§ 48-101-401.

Financial institutions must notify a charitable beneficiary of their beneficiary status within 10 days of the financial institution being notified of the account owner’s death. Financial institutions are prohibited from requiring PII from charity employees. Charitable beneficiaries shall not be required to open a new account with the financial institution.

Charitable beneficiaries may obtain their entitlement by submitting the following documents:

Affidavit that includes the following information

Decedent’s name and last known address;

Description of property if known;

Charity name, address, contact information;

Statement that the beneficiary is a charity;

Request that the property be paid or transferred to the charity;

Statement that there is no other individual or entity entitled to the property;

Signature of authorized individual,

Statement that the affidavit information is true and correct.

IRS Tax Exempt Letter

Certificate of Existence from Secretary of State

Proof of death

W-9

Corporate resolution confirming authority of affiant to action on charity’s behalf

Upon receipt of an affidavit and accompanying documentation from a charitable beneficiary, financial institutions shall distribute held property within forty-five days and must provide requested information about the held property within thirty days. Charities shall not be required to open a new account with the financial institution or provide personal information from any person employed by the charitable beneficiary.

Documentation required:

Affidavit including the following information:

The decedent’s name and last known address;

A general description of the property;

The charitable organization’s name, address, and primary contact information;

Statement that the charitable organization is a charitable organization;

Request that the property be paid, delivered, or transferred to the charitable organization or that information about the property be given to the charitable organization;

Statement that the charitable organization is entitled to payment, delivery, or transfer of the property;

Statement that the affidavit has been signed by a duly authorized representative of the charitable organization under penalty of perjury before a notary public; and

Statement that the information in the affidavit is true and correct.

IRS Tax Exempt Letter

Certificate of Existence from Secretary of State

Proof of death

Corporate resolution confirming authority of affiant to act for charity

W-9

For any charity that has been frustrated trying to collect a clearly bequeathed gift from a financial institution, these laws generally represent a significant increase in protections and clarity.

Illinois, Missouri, and California have bills currently before their legislators, and coalitions are already forming in other states to plan for next year’s legislative cycle. It is only a matter of time before additional states sign new RIFT bills into law.

What Charities, Attorneys, and Advisors Should Do Now

Of course, as with any new law, it may take some time to see how these are actually treated. As non-profits begin to cite these new laws and the financial custodians respond, we will gain clarity and have more definitive answers for what should be done.

But in the meantime, here are some recommendations for charities, estate planning attorneys, and advisors interested in maximizing gifts and honoring donors’ intent.

If you are a nonprofit headquartered in one of the above states, you should review all of your pending beneficiary designation, POD, and TOD matters (IRAs, 401(k)s), and other financial accounts).

Prepare the documentation that financial custodians require in the above states to make distributions to charitable organizations. IRS Tax Exempt Letters, W-9s, Corporate Resolutions, and Certificates of Existence from the Secretary of State should all be available to the organization’s bequest management teams.

Even if your organization is not headquartered in one of the above states, consider testing these new laws to see what the large financial custodians who operate in all 50 states will say when the new law is cited.

Colorado’s 60-day clock starts upon proper written notice from the charity to the financial custodian. Most of the RIFT laws have a similar provision. Make sure you have a plan in place for submitting an affidavit and notifying the custodian, in particular who is responsible for doing that at your organization. This will help you move quickly when accounts are identified.

Monitor the financial institutions to ensure compliance with these new laws. As with any new law, enforcement will be the proving ground. Document any resistance you encounter.

Is Your Charity Struggling with PODs?

The POD problem and the new RIFT laws illustrate the importance of monitoring and responding promptly to developments in case law, legislation, and state and federal rules. This is not a simple task. Navigating the legal landscape and taking appropriate, timely action is one of the most important reasons to partner with CCK Bequest Management.

Over 25 years of legal experience, a national practice, and our deep roots in the planned giving community have given us tools to offer to organizations like yours. We assume full responsibility for realizing matured bequests — protecting and collecting the full intended gift, preventing diminishment, loss, and delay.

If you are unsure if you are prepared to fully realize donors’ intent and maximize planned gifts to your organization, then please reach out to our firm at 401-336-7770 or cckbequest.com/contact/.