Blog

Rejecting a Bequest: When, Why and How to Say “No Thank You” Part 2

February 28, 2022

Organizations may be unenthusiastic about rejecting bequests for various reasons. Some may fear that it is rude to do so. Others may believe that there is recoverable value in any gift. There are certainly charities, doubtless in the minority, that are unaware of the “right to refuse.”

In this two-part post, we will explore some of the legal, ethical, and tactical issues that arise in a refusal situation.

From the charity’s perspective, there may be one or two opportunities to reject a bequest, one during the cultivation process and one after death.

Sometimes, a living donor may announce their intention to leave a certain testamentary gift to an organization. For one reason or the other, the gift may be undesirable or unworkable.

Consider the situation of a charity dealing with abandoned pets. Testator John Doe wishes to leave his mansion in Beverly Hills as a refuge for the animals. The mansion was built in 1927 for a movie star and has been preserved meticulously ever since. The charity needs to think about the ongoing costs of maintenance, renovations for the new purpose, and all other costs associated with a century-old palace. Doe, on the other hand, expects the charity to stretch its already slender budget to cover the added financial burden.

The charity might acquiesce to Doe’s plan during his lifetime, hoping to be able to wiggle out of the restriction (or sell the property) during probate. However, a better approach for the organization would be to meet the situation head-on and engage Mr. Doe in frank discussions about the problem. True, there is the risk that he will revise his estate plan to the charity’s detriment, but isn’t that to be preferred to the deceptive act of feigning agreement with his estate plan while plotting to thwart it post-mortem? Don’t industry standards and basic ethics demand that Doe should be informed of the charity’s reservations and limitations?

CCK TIP: It will often be easier to deal with a donor like Mr. Doe if the charity can point to a pre-existing gift acceptance policy that provides “cover” for the reluctance to accept a planned gift. Ideally, the policy would have been available to Mr. Doe (by, e.g., being posted on the charity’s website, even if he did not see it) during the estate planning process. This way, the donor will know that the charity has thought about and addressed these issues in a reflective manner. Ideally, the policy will contain general “escape” clauses such as the following: “Absent extraordinary circumstances, Organization will not accept bequests that entail significant ongoing expenses that are not covered by the gift.”

CCK interacts with gift planners on a regular basis. It is our impression that in many cases, a donor can be persuaded to modify a restricted gift in a way that serves her philanthropic interests while accommodating the situation of the charitable beneficiary.

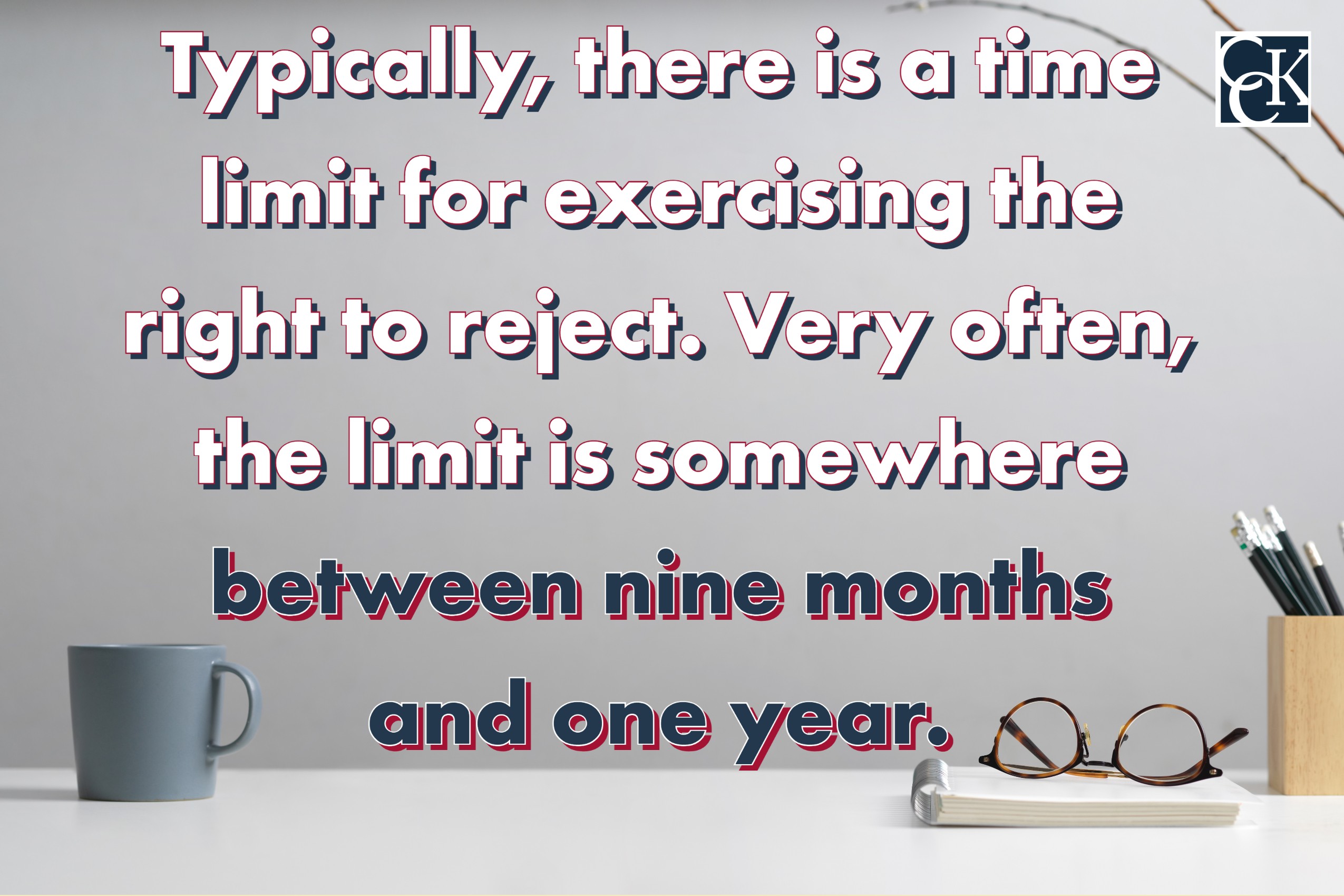

Most frequently, the question of refusing a gift arises from a “surprise” bequest that is revealed only after the testator’s death. In every state, there is a procedure in place for rejecting a gift. Typically, there is a time limit for exercising the right to reject. Very often, the limit is somewhere between nine months and one year.

This “limitations” period usually does not present an absolute bar to later rejections. For example, under the pertinent California statute, the nine-month period is described as an interval during which the declination of a bequest gift is “conclusively timely,” implying that later refusals may or may not be timely depending on the circumstances.

Let us therefore suppose that Mr. Doe’s bequest described above became known only after his passing. In such a situation, the charity would be able to decline the gift by informing the executor. In all likelihood, the executor would require a writing to deposit with the court.

Some may wonder if there is any possibility of altering the conditions of the gift in the post-death environment to make it more palatable to the charity. If the gift was made by will, there is little chance of modifying conditions or restrictions unless the charity can demonstrate to the court that the limitations are impossible in general (i.e., not just for a particular charity) or offensive to public policy (such as an express directive that the bequest cannot be used for a particular racial group).

There may be more of a chance to modify a restriction in a gift made by trust. Since testamentary trusts are administered without court supervision, the trustee is sometimes vested with, or just exercises, considerable discretion. In these cases, a frank and open discussion with the trustee can often lead to a satisfactory resolution and allow the charity to avoid rejecting a valuable gift.

Usually, a trustee will have broad discretionary powers if and only if the trust instrument so provides. Less frequently, such powers may be granted to the executor of a will. Either way, a charitable beneficiary facing an accept-or-reject dilemma will not be able to assess practical solutions unless and until it is in possession of a copy of the testamentary instrument. While this is usually not an issue in the case of a will, the right to trust documents varies from case to case and from state to state.

Before making a “blind” decision whether to accept or reject a potentially valuable gift, a charitable beneficiary or its counsel should “go the extra mile” to ensure that it has obtained every bit of information relevant to that determination.

CCK TIP: One of the biggest mistakes that charities make in bequest management is neglecting to obtain, and analyze, the testamentary instrument. Some of the most intractable probate problems may disappear when that document is reviewed.

February 20, 2023